The following article is a summary of the OECD-FAO Agricultural Outlook 2025-2034 section on marine ingredients. The original paper is available from: https://doi.org/10.1787/601276cd-en

Consumption of global seafood is expected to increase, with most of that growth occurring in Asia and Africa. This includes only a slight increase in per capita consumption from 21.1 to 21.8kg. Aquaculture will continue to be the main driver of global seafood production, increasing to 56% of the global supply of more than 200 million tonnes by 2034. Despite this growth and maintenance in demand, the global prices of seafood are expected to decline in real terms.

Exports of seafood are expected to grow, albeit at a slower pace than previous decades. Furthermore, increasing uncertainties face the sector, including changing environmental conditions which impact global production and geopolitical tensions impacting trade policies. Improvement in global fisheries management offers some respite, while a growing focus on sustainable practices will continue to dominate further development of aquaculture.

Fishmeal and fish oil

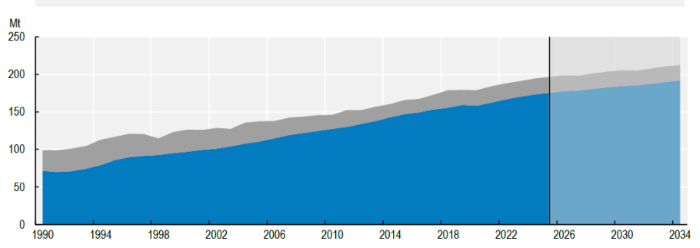

Marine ingredients have long been considered strategic feed ingredients to global aquaculture production. Of the 21 million tonnes (live weight) of fish products utilised for non-food uses in 2034, 83% are projected to be used for fishmeal and fish oil production. The remaining 17% is likely to be made up of other nonfood uses such as for ornamental fish, fingerlings, bait, pharmaceutical goods or as trash-fish use in parts of the world (Figure 1)

Fishmeal will continue to be used primarily as a strategic ingredient in aquaculture feeds, and by 2034, 84% of global fishmeal production will be used by this sector as feed, compared to 78% in the base period of the OECD-FAO study (2022-2024). China will continue to be the largest aquaculture producer, and with this also the largest consumer of fishmeal. OECD-FAO estimates that China will account for 42% of world fishmeal

consumption by 2034.

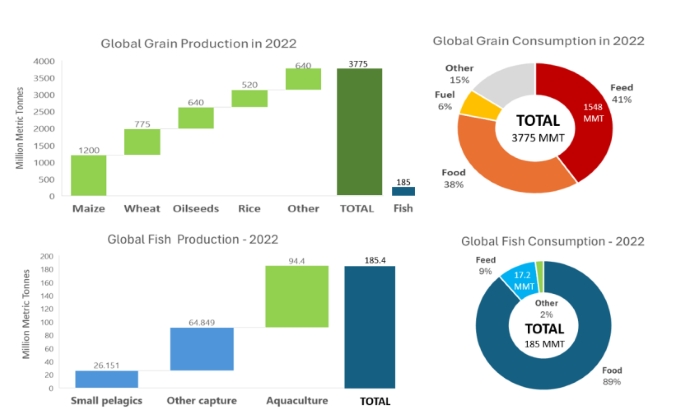

Although fishmeal is mainly used as a feed ingredient by the aquaculture sector, fishmeal is not the main feed ingredient used by that sector. Other feed ingredients, mostly agricultural products such as soybean meal, wheat, rapeseed and corn will continue to make the largest contribution to nutrient supply in feeds for the sector in the foreseeable future. Fundamental differences in scale (3,775 million tonnes grain production versus 6 million tonnes of fishmeal and oil production in 2022 – Figure 2) explain the rationale for this, along with there being limited capacity for any

major fishmeal and fish oil production increase. The OECD-FAO study forecasts that by 2034, the use of ingredients such as soybean meal in aquaculture will reach 11 million tonnes, whereas fishmeal inclusion in aquaculture feeds will increase to 4.9 million tonnes.

Consumption of global fish oils shows a different story of growing competition between aquaculture and dietary supplements for human consumption. Forecasts suggest that by 2034, nearly 60% of fish oil (0.9 million tonnes) will be utilised by aquaculture. Farmed salmonids will be the largest aquaculture consumer, with salmonid producing nations like Norway, Chile, Turkiye, and UK continuing to be the main consumers. The remaining 40%+ will be consumed mostly by direct human consumption (pharmaceutical) and pet food applications.

The OECD-FAO study predicts that the quantity of capture fisheries production that is made into fishmeal and fish oil will show an upward trend in the next decade, compared to the previous decade. While the total volume will vary between 15 million tonnes in El Niño years and 17 million tonnes during peak fishing years, the total fishery resource used for direct rendering (forage use) remains well below the 26 millions tonnes of fish which which were used in the 1990s.

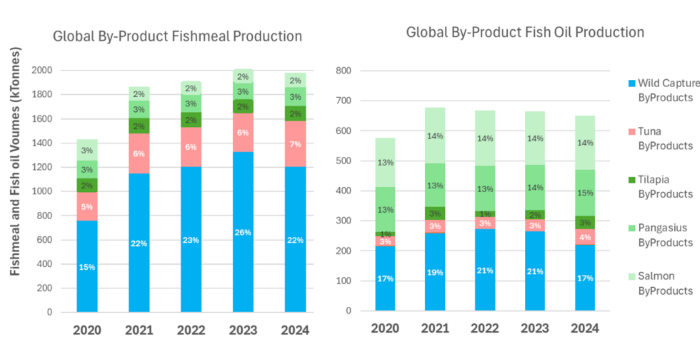

Global production of fishmeal and fish oil is projected to reach 5.9 million tonnes and 1.5 million tonnes by 2034, respectively, representing a 12% increase for both ingredients compared to the base period. Much of this increase is likely to come from fish by-products, with their use in fishmeal production steadily rising over the past decade reaching almost 40% (2 million tonnes) of total production in 2023 (Figure 3). This is likely to continue, driven by the growing demand for fish fillets by consumers, which generates more by-product resource for marine ingredient production. For fish oil, the proportion sourced from by-products exceeds that of fishmeal due to the high oil levels in the waste streams from some aquaculture production sectors (e.g. salmon and pangasius). More than 54% (0.66 million tonnes) of all fish oils came from by-products in 2023. This growth is expected to continue albeit at a slower pace in the next decade.

The OECD-FAO study projects that global exports of fishmeal will rise by 8% relative to the base period, reaching 3.8 million tonnes by 2034. The world’s largest fishmeal exporting country, Peru, is expected to record one of the highest growth rates over the next decade, driven largely by a rebound from the unusually low export volumes recorded during base period of the OECD-FAO study, when it experienced a very strong El Niño event.

China will continue as the dominant global fishmeal importer, accounting for more than half of all imports by 2034. This reflects the growing demand from its aquaculture sector. In contrast, fishmeal imports from other traditional importing countries, such as Norway and the European Union (EU), are projected to decrease as China takes a growing share of production.

Exports of fish oil are forecast to increase by 9% by 2034. Peru, Viet Nam, and Europe will lead global exports of fish oil. In Viet Nam, exports of fish oil will primarily consist of used cooking fish (pangasius) oil exported to the US, where it competes in price with used vegetable cooking oil. The EU, Norway and the United States will remain the primary importing markets over the next decade.

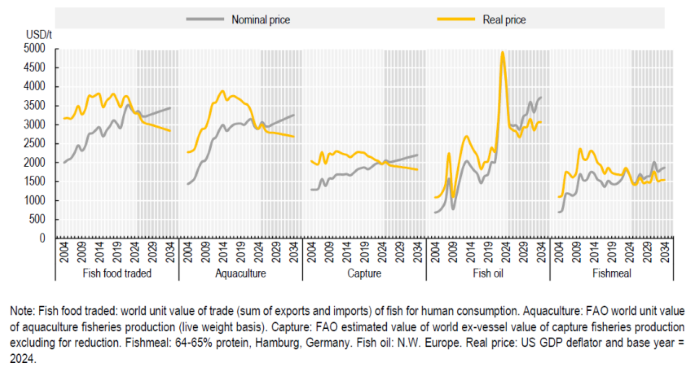

Prices of fish oils are expected to decline in both nominal (-7.5%) and real (-26%) terms over the next decade, reflecting the unusually high prices in the base period (Figure 4). These high fish oil prices during the base period (2022-2024) were caused by combination of unusually low harvests of anchoveta in Peru associated with the 2023 El Niño event and high global vegetable oil prices.

The OECD-FAO study predicts the price of fish oil to decline until 2028 in real terms before returning to its historic trend of slow growth due to continuing demand from aquaculture feed and human consumption demands. Prices of fishmeal over the next decade are projected to increase in nominal terms (10%) but decline in real terms (-12%). The real term decline is projected to be significantly lower than in the previous

decade, when prices declined 24% from their historic peak in 2013-14. A continued decline in fishmeal prices is forecast in the short-term before settling into their historic pattern of remaining relatively stable on average but with potential price movement due to any El Niño event impacts that may occur over the coming decade. Overall, the future for marine ingredients looks to be steady and transitioning. Growth over the next decade will be limited (~12%), and likely to continue to be affected by global climatic weather like El Niño events. Increasingly the sector will transition from relying on whole wild fish to more use of fish by-product streams, serving an important role in the circular food economy as it seeks to retain important nutrients within our foodsystem.

Consistent with trends over the past decade, aquaculture feeds will become increasingly reliant on grain products to supply most of their nutrients, while marine ingredients will continue to play a strategic role.