Global shrimp production was expected to rise in 2025 with key producers such as Ecuador leading growth, while Asia showed a modest increase with variations across countries. China’s output was projected to decline due to disease and regulatory restrictions. The overall outlook points to expanding supply but highlights regional disparities and challenges.

Global production is up in 2025 Shrimp production in 2025, driven by Asia and Latin America, is expected to increase moderately compared to 2024. At Shrimp Summit 2025, held in June in Bali, Indonesia, the Kontali team predicted that vannamei shrimp production will rise to 5.84 million tonnes, reflecting a 6% growth from 5.5 million tonnes in 2024.

In October, at the Responsible Seafood Summit 2025 in Cartagena, Colombia, RaboResearch and the Global Seafood Alliance (GSA-Rabobank) presented results of the survey on global vannamei shrimp supply. Production is expected to grow only 2–3% in 2025 to 6.1 million tonnes. The survey reported a 4% increase in global supply of the black tiger shrimp led by Vietnam, China, India and Bangladesh.

A global view on supply from top producers

Growth forecasts on Ecuador’s production in 2025, included Gorjan Nikolik’s (RaboResearch) at 15%. At TARS 2025, held in Chiangmai Thailand, in August, it was an almost 18% indicative growth reaching 1.75 million tonnes, by Vitapro’s Pablo Montalbetti Gómez de la Torre. At the Global Shrimp Forum (GSF 2025) Sandro Coglitore, Omarsa clarified that 2024 was a flat year for Ecuador as it was in a consolidation process. Farms that had changed hands were brought back online and

resumed production in 2025. A notable surge in growth in 2025, is expected to continue into 2026. Numerous farms are still undergoing ownership changes, which will impact the industry’s dynamics Ecuador’s shrimp industry continues to be the “idol” with 3-phase models: low stocking density (relative to that in most of Asia), nursery systems and almost 4 cycles/year. The news from Ecuador is that large farms buy up smaller farms, and they are increasing stocking density in low saline areas to 25-30 PL/m2 and even as high as 40 PL/m2.

GSA-Rabobank had forecasted a 2% growth in Asian production for the year 2025. The general view is a declining production in Southeast Asia while India’s production is stagnant. Some trends suggested rising volumes for India (5.0%), lower volumes in Vietnam (-2%) and Thailand (-1%). GSA-Rabobank expected no growth in Indonesia and volumes to remain at 350,000 tonnes.

Below are some shared perspectives by local industry stakeholders regarding the situation with both vannamei and black tiger shrimp in 2025.

EHP and regulations restrict production in China

The China Statistical Yearbook reported a 2025 production of 2.37 million tonnes of vannamei shrimp. Amber Chen, Nutriera, China noted that 1.53 million tonnes were from saline systems and some 880,000 tonnes came from freshwater farming. Several industry players provided lower estimates. FuCi Guo, MSD Animal Health suggested around 1.7 million tonnes of shrimp production and vannamei accounted for 88%. Most domestic shrimp are consumed domestically and generally of smaller size. Farmers adjust their plans and shift to alternative species, based on price signals and import surges, said Louis Zhou, HuaXin Food Group, at GSF 2025.

Industry also expect lower volumes in 2025 compared to 2024, due to stricter regulations on groundwater use and wastewater discharge enforced by both local and central authorities, slow down in local government investment in greenhouses and Enterocytozoon hepatopenaei (EHP) outbreaks. Guo said intensive farming in small greenhouses emerged as the main strategy for increasing production but lately small greenhouse farms in Jiangsu and Shandong have closed. Back in 2024, 450,000 of these 0.4ha greenhouses, were expected to contribute 450,000 tonnes/year.

Managing EHP well in India

A recent 2025 Society of Aquaculture Professionals (SAP) crop review reported production rising to 1.05 million tonnes, with 989,000 tonnes of vannamei and 60,500 tonnes of black tiger shrimp, according to SAP President Saji Chacko. During a SAP session at World Aquaculture 2025 India in November, higher output was anticipated in all regions, especially the

west and north at 10-15%.

There have been production improvements over the past three years due to changes in stocking density. Multiple partial harvests—from shrimp size 100/kg down to 60, 40 and finally 20/kg —have boosted farmer profits, with some achieving three cycles annually. Nursery rearing also contributed to these gains. EHP was a persistent issue for over three years, but Indian farmers reportedly managed it in 2025, through crop cycle adjustments and selecting suitable post larvae from various broodstock lines, according to Ganesh Moorthy, CP India. With multiple genetic lines now available, farmers are eager to verify the specific line of purchased post larvae (balanced, fast, or hardy).

In southern India, some farms start with a vannamei crop, followed by black tiger and then a vannamei crop again. Almost 30-40% of farms achieve five crops in two years. The stocking density for vannamei shrimp was 40- 60PL/m2.

A priority in India is building its domestic market. Since processors prefer to focus on exports and offer little support, farmers are creating their own local fresh markets at the district level. According to Ganesh, domestic consumption has grown.

TPD, disease and high costs in Vietnam

The feed industry in Vietnam was clear that there was a gradual recovery compared to the prior year in vannamei shrimp production, but estimates on volumes differed from 470,000 to 600,000 tonnes. Export vs domestic market ratio is 70:30. The domestic sector remains significant for risk-averse farmers, absorbing fresh and mid-size shrimp grades with greater price volatility.

In the first quarter 2025, translucent post larvae disease (TPD) posed significant challenges at the hatchery and grow-out stages, according to Chewen Wei, Uni-President Vietnam Co Ltd. “Farmers lost confidence, which led to delayed pond stocking and lower stocking densities. Stocking activities gradually normalised from April. These Q1 delays affected overall annual production,” said Wei. “Persistent disease and environmental issues discouraged pond restocking,” said Ton That De, Viet Uc at GSF 2025. He added that lower farming success rates with survival rates down to 50% were attributed to higher density farming practices. With these risks, together with other challenges and rising costs, some have opted for fast growth genetic lines to harvest as fast as possible. In the Mekong Delta, structural transformation occurred in 2025, reported Wei. These included improved pond infrastructure, enhanced water treatment systems, advanced management practices, and risk segmentation strategies. Both farming success rates and production stability improved in key areas. Ton estimated that soon the ratio of small farms: large farms will shift to 70:30 from the current 90:10.

Continuous low volumes in Thailand

Official data from the Department of Fisheries (DOF) showed a 0.7% decline for vannamei shrimp production to 232,807 tonnes. Industry sources gave a higher estimate of 380,000 tonnes.

“Flooding in the south caused crop losses of 10–30 tonnes per farm, while cold weather in central Thailand brought down temperatures to 23-24°C and led to white spot syndrome virus (WSSV) and yellow head virus (YHV) outbreaks and reduced feed intake,”

said Soraphat Panakorn, President, Thailand Aquaculture Business Association (TABA).

Indonesia: Pushing boundaries

As production fell in Q4 2025, a 25-30% decrease was projected for 2025 to only 230,000-245,000 tonnes. Haris Muhtadi, CJ Feed & Care, Indonesia cited EHP and AHPND as major causes of decline in farm productivity. He added that for some farmers, the key problem was high stocking densities. In Indonesia, low density is <80 PL/m2; median 80-150 PL/m2 and high >150 PL/m2 (Shrimp Outlook, 2025). In East Java, farm output improved when farmers lowered stocking density by 10-15%. They improved water quality by extending water supply intake lines from 400-500m to 1,000m.

At Shrimp Summit 2025, Haris stressed how over the last ten years, farms managed cash flow with several partial harvests, starting from 60 days until the final harvest at 115-120 days. To maintain carrying capacity, intensive farms may have 3-5 of partial harvests, periodically or when dissolved oxygen goes below 4ppm and biomass is 300-400kg/HP. “We are “pushing the environment” which is not sustainable,” said Haris. New farming areas in the eastern part of the archipelago are being exploited when areas in Sumatra and Java are exhausted, allowing for yields of 50-60 tonnes/ha/crop in new farms as compared to 20 tonnes/ha/crop in the older farms

Veering towards farming black tiger shrimp

The GSA-Rabobank Summit Survey 2025 noted that “Asian farmers are switching back to black tiger shrimp in search of better prices and farm profitability”. Data showed an increase of 4% to around 650,000 tonnes, led by Vietnam at 200,000 tonnes. McIntosh gave estimates of only 538,000 tonnes for 2025 (Table 2).

“In India, black tiger shrimp output has been rising and can be expected to increase in 2026,” said Ganesh. Driving India’s black tiger farming revival are broodstock from Unibio (Madagascar) and Moana (USA) as well as the locally developed Nicobar line by RGCA- Rajiv Gandhi Centre for Aquaculture. CP India is using this local line to produce 150 million PL in 2025, and targets 400 million PL in 2026. Recently, Unibio has emerged as a leading producer, with around 2.4 billion PL in 2025. It is expected to produce 3.0 billion PL in 2026. The stocking density was 7-10PL/m2 rising to 20PL/m2. In October, farmgate prices in Andhra Pradesh, India, for size 30/kg vannamei shrimp was USD4.71/kg versus USD5.5/kg for black tiger shrimp.

Thailand’s 2025 production of black tiger shrimp rose by 23.4% to 19,589 tonnes (DOF, 2025), as vannamei farmers struggled with challenges on choosing suitable genetic lines and reliable post larvae quality, prompting many to switch species. In 2025, Malaysia’s total production was 42,000 tonnes at 60:40 vannamei: blacktiger shrimp. As farmers faced issues with vannamei post larvae, many shifted to farming the black tiger shrimp.

Farmgate prices

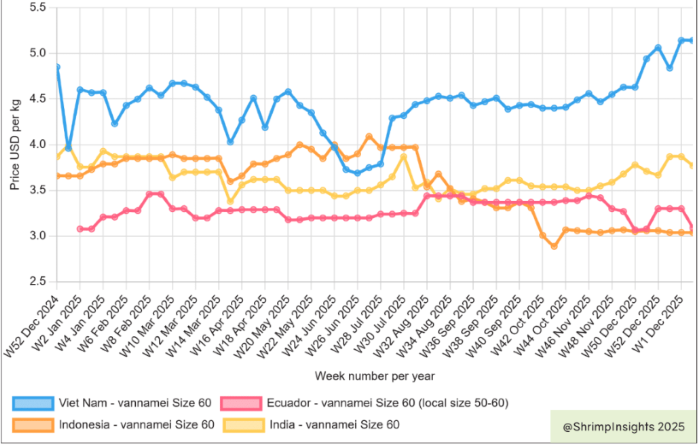

In 2025, Vietnam led with the highest farmgate prices for size 60/kg vannamei shrimp. There was, however, extreme volatility, linked to supply issues. At year-end, Vietnam had the highest USD price per kg at 4.84,followed by India (3.87), Ecuador (3.09), and Indonesia(3.04, Figure 1).According to industry, farmgate prices reflected production dynamics arising from disease outbreaks. Due to price differences, Shrimp Insights reported that YTD September, India exported 50,500 tonnes to Vietnam, likely for reprocessing. Indonesia already had the lowest farmgate prices and in August, the caesium-137debacle, lowered these further, from USD3.97/kg toUSD2.89-3.04/kg. JALA also reported lower prices(USD2.43-2.55/kg) since October.

Reactions on tariffs and recent market uncertainties Aside from exporting head-on, shell-on (HOSO) shrimp to China, Ecuador’s processors are taking advantage of its low US tariffs (10%) to capture the peeled products market. In July, value added accounted for 31% of exports to date, compared to 28% for the whole of 2024,up from 20% of exports in 2021 (Montalbetti, 2025).The US is Indonesia’s largest and most important market. At the Shrimp Aquaculture Conference 2025(SAC), a panel noted that the industry is not ready to export to the EU because of the latter’s focus on sustainability. By end 2025, Indonesia had pivoted 10% of exports to China (Shrimp Insights 2025). While exports to the US declined by 43%, India increased its exports to China (+33%) and to the EU (+58%). Value addition increased 27%. (Chacko, 2025).

Outlook for 2026: Uncertain for Asian producers

The prospects for Asian shrimp producers in 2026 remainun certain and highly variable across the region. An industry source expects Indonesia’s production to exceed 300,000tonnes if PT Bahari Makmur Sejati (BMS Foods), the Indonesian food processor which was flagged by the USFDA for Cs137 contaminated shrimp exports, resumes operations in early 2026.

India has reached a production milestone of one million tonnes, according to SAP. However, India must focus on increasing domestic consumption, which currently stands at just 100,000 tonnes, with a target to reach 30% of total production by 2030.

India and Indonesia have a major regulatory hurdle. Both countries are not in the approved list regarding the control on antibiotic use under the EU Regulation (2023/905).This requires all exporting countries to be in the list by 3September 2026. Failure to be included on this list will block exports of animal-origin products, including shrimp and fish, to the EU.

Vietnamese exporters must contend with a new non-tariff barrier in the EU and UK. From 2026, major retailers will require stricter animal welfare standards. Specifically, shrimp must be completely stunned, typically through electrical methods, prior to ice immersion—replacing the traditional cold-shock approach. Leading UK retailers such as Tesco, Marks & Spencer, Sainsbury’s, and Waitrose have already integrated these requirements into their procurement policies, making compliance essential for maintaining approved supplier status.

After 13 years of stagnant production, the Thai Shrimp Association has urged the government to declare a ‘National Agenda’ – recovery of the shrimp industry and to target 400,000 tonnes in 2026. Thailand’s shrimp production peaked at 600,000 tonnes in 2011 but dropped by half in 2013 due to early mortality syndrome (EMS) or AHPND outbreaks.

Ekapoj Yodpinit, president of the association has two objectives. An opportunity for Thai shrimp to capture the US market from India, since Thailand’s tariff is only19% as compared to India’s 58%. Accelerating free trade agreements with the EU, UK and Korea could recover 60,000 tonnes of lost export after Thailand lost privileges under the Generalised System of Preferences(GSP) in the EU in 2015 and recently in 2020 in the US.

In summary, 2026 will present a complex and evolving environment for Asian shrimp producers, shaped by stagnant or uneven production growth, uncertainties with tariffs, shifting export strategies, and increasingly stringent regulatory requirements in key markets.

Reference Shrimp Insights (2025).https://www.shrimpinsights.com/price-portal